The Kelly Criterion: Optimizing Bet Size with Math

You can get a bet right and still lose money.

That’s exactly what the Kelly Criterion helps you solve.

If you want to understand what it is and see how it works step by step, you’re in the right place.

What the Kelly Criterion is really about

Before getting into formulas, let’s keep it simple.

Every time you place a bet, there are two decisions:

- What you bet on

- How much you bet

Most people focus only on the first one.

That second decision is where a lot of money is won or lost.

The Kelly Criterion is just a way to answer that second question properly.

So what does it actually do?

It gives you a percentage.

Not a random number, not a guess — a percentage based on:

- The odds

- And how likely you think the bet is to win

That percentage tells you how much of your bankroll to use.

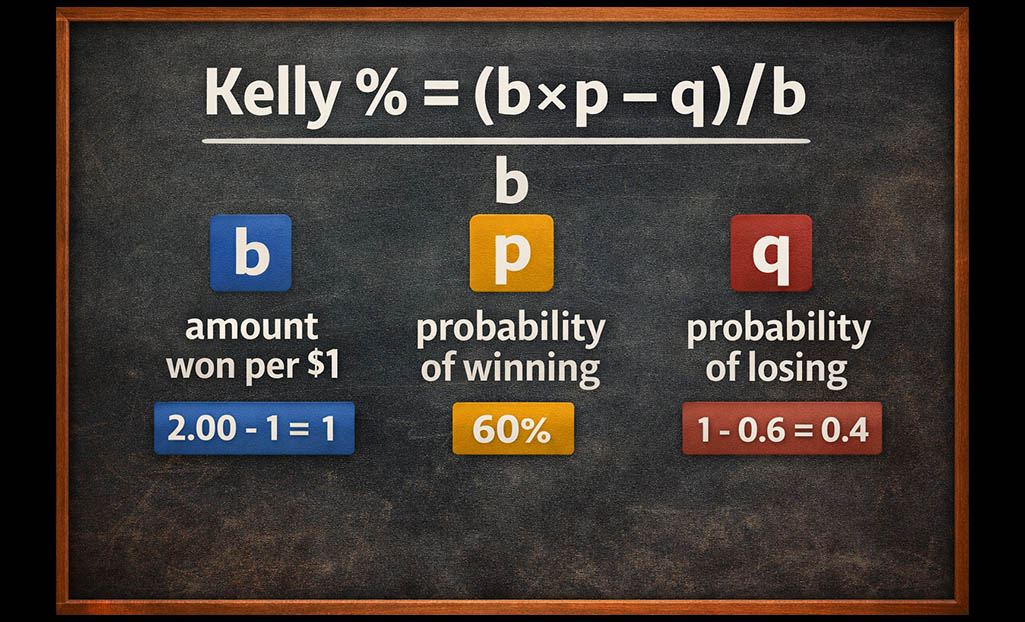

The formula

Kelly Criterion formula explained step by step with a real betting example

At first glance, this looks confusing, but each part is simple.

Let’s break down where everything comes from:

- b → how much you win per $1 (based on odds)

- p → your probability of winning

- q → your probability of losing

And q is just 1 - p, so nothing new there.

Now let’s walk through a real example

Say you’re looking at a bet with:

- Odds: 2.00

- You think it wins 60% of the time

Now we go step by step.

Step 1: Convert the odds into "b"

Odds are 2.00.

That means:

- You get your money back

- Plus the same amount as profit

So the profit part is 1

That’s why b = 2.00 - 1 = 1

Step 2: Set your probabilities

You believe the bet wins 60% of the time:

- p = 0.6

- q = 0.4 (because 1 - 0.6 = 0.4)

Step 3: Put everything into the formula

Now we just replace the values:

Let’s go line by line:

- 1 × 0.6 = 0.6

- 0.6 - 0.4 = 0.2

- Divide by 1 → still 0.2

What that number means in real life

0.2 = 20% of your bankroll

So if you have:

- $1,000 → bet $200

- $500 → bet $100

This is where everything connects.

What happens if the number is negative?

Let’s look at another case.

- Odds: 1.80

- You think it wins 55% of the time

We do the same steps:

- b = 0.8

- p = 0.55

- q = 0.45

Now calculate:

- 0.8 × 0.55 = 0.44

- 0.44 - 0.45 = -0.01

- Divide by 0.8 → negative result

And this is important.

Even if it feels like a decent bet, the numbers don’t support it.

Why people don’t use this and why it matters

Most people don’t calculate anything.

They:

- Bet more when they feel confident

- Bet less when they’re unsure

- Change amounts constantly

The problem is that this creates inconsistency.

The Kelly approach keeps things aligned with the actual quality of each bet.

A more comfortable way to use it

Betting the full percentage can feel like too much sometimes.

That’s why many people adjust it.

This keeps the same logic, just with less risk.

One thing you need to be careful with

Everything depends on your probability. If your estimate is wrong, your result will be wrong too.

So the formula works best when:

- You have a solid idea of your probabilities

- You’re consistent with how you estimate them

Bringing it all together

At the end of the day, this isn’t about predicting better.

It’s about handling your bets in a more controlled way.

Instead of:

- Guessing amounts

- Following feelings

You’re using a simple structure that connects:

- Odds

- Probability

- And bet size

And once that starts to make sense, your decisions become a lot more consistent.